Less Is More

John Lekas – CEO & Senior Portfolio Manager

March 12th, 2026

Markets entered the year expecting interest rate cuts from the Federal Reserve. Instead, we are seeing a different picture emerge globally. Both Australia and the European Union are preparing to raise interest rates, underscoring a reality we have emphasized for the past several years: inflation is a difficult force to eliminate once it becomes embedded in the economy.

Initially, inflation manifested primarily through wage pressures. Today, we are increasingly seeing price inflation across the broader economy. Recent geopolitical developments in the Middle East, combined with a relatively weak dollar policy, have further intensified these inflationary pressures.

Markets have recently experienced increased volatility, particularly within private credit. Much of the recent damage has occurred within the software sector. In our view, the magnitude of this decline appears overdone, and we believe that attractive buying opportunities may soon emerge for long-term investors as fundamentals stabilize. Recent research from Morgan Stanley suggests the current stress is more likely a repricing of risk rather than the beginning of a systemic credit crisis.

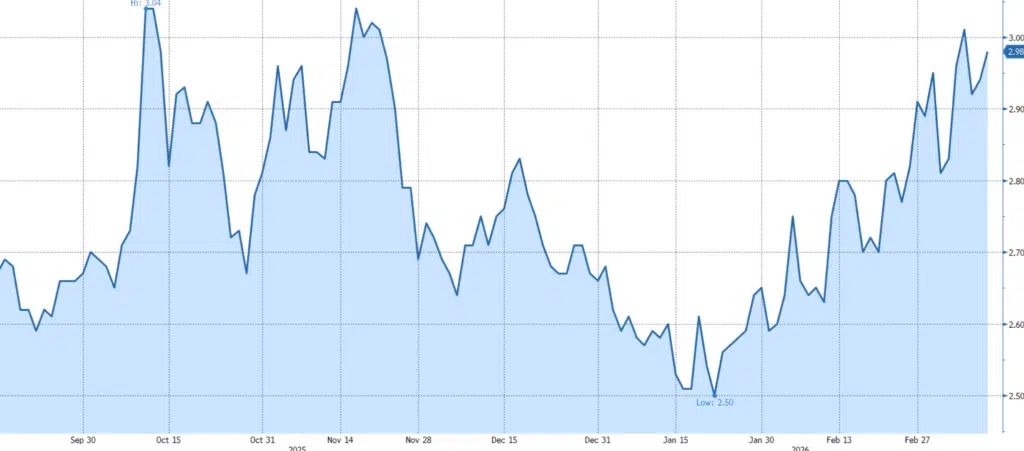

Credit spreads have widened by approximately 50 basis points YTD in both high-yield and investment-grade markets. However, the CLO market—particularly new issuance rated BBB and above—remains relatively tight. Overall, both high-yield and investment-grade credit spreads continue to appear compressed relative to underlying risks.

High Yield Credit Spread

Investment Grade Credit Spread

Our guiding principle remains straightforward: less is more. Maintaining discipline and avoiding excessive risk allows investors to take advantage of opportunities when markets temporarily overshoot to the downside.

- The High Quality Fund will remain tightly positioned.

- The High Yield Fund is managed with the objective of generating income consistent with BB+ credit quality and low duration.

Our current expectations for rates in 2026:

- 10-Year Treasury Yield: 4.5%

- 30-Year Treasury Yield: 6.0%

- Federal Reserve Policy: Uncertain; rate cuts or hikes remain possible

Overall, we expect elevated volatility throughout 2026 as markets continue to navigate inflation dynamics, geopolitical uncertainty, and evolving monetary policy. In a worst-case scenario, the VIX potentially could revisit its April 2025 highs in the 60s range.

For Financial Professional Use Only – Email not for Public Distribution Source:

Investing in any mutual fund involves risk, including loss of principal. The risks specific to the Leader Funds are listed on the attached Fact sheets and detailed in the prospectuses for the funds. There is no guarantee the funds will achieve their objectives. Expense ratios are as of the 11/28/2025 Prospectus.

An investor should consider the Fund’s objectives, risks, charges, and expenses carefully before investing or sending money. This and other important information can be found in each Fund’s prospectus. For more information, please call 1-800-269-8810.

Please read the prospectus carefully before investing.

Current Yield is the weighted average of the annual rate of return based on price. It is calculated by the coupon divided by the price. Average Yield-to-Maturity is the weighted average of the percentage rate of return if the security is held to maturity. Leader Capital Corp. serves as adviser to Leader Short Term High Yield Bond Fund, and Leader High Quality income Fund, The Funds are distributed by Matrix 360 Distributors, LLC, Member FINRA/SIPC. Leader Capital and Matrix 360 are not affiliated.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Share prices and investment returns fluctuate and investor shares may be worth more or less than the original cost upon redemption. To obtain performance as of the most recent month-end, please call 1-800-269-8810.